Iran War Stalemate: What Signal Should the Market Follow?

Original Title: The Bond Market Is Flashing Red, The Next "Phase" Of the Iran War

Original Author: The Kobeissi Letter

Translation: Peggy, BlockBeats

Editor's Note: Against the backdrop of escalating geopolitical conflicts, the market's focus is quietly shifting. Initially, discussions centered around oil price shocks and the Middle East situation, but as the war reached a stalemate, a more systemic variable began to emerge: financial conditions themselves are tightening.

The core argument presented in this article is that what is truly driving the current market is no longer the war itself but rather the disorder in the bond market.

Over the past month, the U.S. 10-year Treasury yield has risen rapidly, directly reshaping rate expectations from a "rate cut path" to a "rate hike reconsideration," suppressing the stock market, commodities, and policy space. During this process, the ongoing weakness in the labor market and the renewed rise in inflation expectations have exacerbated the Fed's dilemma.

Of greater concern, the author places this round of market volatility within the policy response function: as yields approach the "policy shift range" of 4.50%–4.70%, the probability of government intervention will significantly increase. Whether it's historically pausing tariffs or recent shifts in "peace negotiations," these events are interpreted as specific manifestations of bond market pressure transmitting to the policy level.

This also raises a deeper question: as the bond market begins to dominate asset pricing and policy rhythm, what signal should market participants follow? Geopolitical narratives or marginal changes in the interest rate curve?

In this structural shift, this article attempts to provide a clear answer—keep an eye on the bond market. Because it not only reflects risk but also determines the boundaries of risk.

The following is the original text:

As the peace negotiations of the Iran war stall, an urgent question is emerging in the U.S. market: the bond market is "malfunctioning." Amidst the intense turmoil in the bond market, we believe the probability of "intervention" is rapidly rising. What does this mean? Let's explain below.

Before we begin, we suggest you bookmark this article, as it will serve as a guide to the market trends in the coming weeks.

When the Iran war broke out on February 28 (starting with the U.S. and Israel's assassination of Iran's Supreme Leader Khamenei), the initial rise in oil prices was less than 15%. The U.S.' assessment at the time was that assassinating Khamenei would quickly lead to a regime change in Iran, resulting in a relatively fast and minimally disruptive outcome. However, fast forward to now, the Iran war has entered its 27th day, Iran has rejected the U.S.' "15-point peace plan," and peace negotiations have clearly stalled.

Currently, it is no longer possible to determine if either party still explicitly desires to end this war. Therefore, the oil price remains elevated, with the WTI crude oil price once again approaching $100 per barrel. However, this is no longer the primary concern facing the market. The real issue has now shifted to the bond market, rapidly evolving into the greatest impediment to the global economy.

Core Issue

During the early stages of the war, the oil price was the market's focal point, and it remains so to this day. The reason is simple: the oil market most directly and swiftly reflects the impact of the war.

But now, the bigger problem is the sudden surge in U.S. Treasury yields.

As shown below, in the 27 days since the outbreak of the Iran war, the U.S. 10-year Treasury yield has risen from around 3.92% to 4.42%, a cumulative increase of 50 basis points. It is important to note that before the war broke out, the market's focal point of discussion was still how many rate cuts would occur in 2026.

U.S. 10-Year Treasury Yield since the Outbreak of the Iran War

The current speed of the rise in the U.S. 10-year Treasury yield, and more broadly, the overall ascent of U.S. bond yields, is roughly comparable to the performance during the "Liberation Day" period in April 2025.

However, this time the backdrop is much more complex, and stabilizing the bond market is far from being as simple as it may seem on the surface. This will soon become the most central narrative in the market.

From Rate Cut Expectations to Rate Hike Pressure

To better understand the intensity of this dramatic shift, one can look back at the market's rate expectations at the end of 2025.

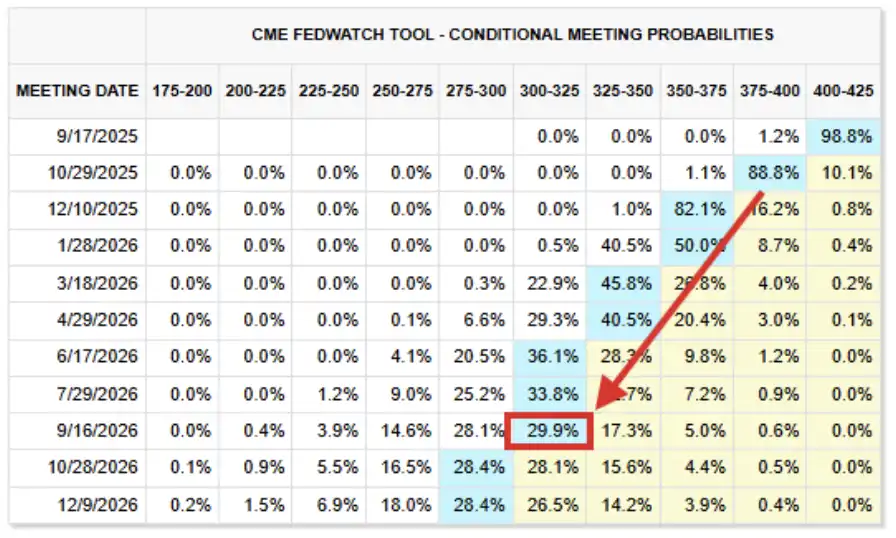

As shown below, the market's "base case scenario" at that time was that by 2026, the Federal Reserve's federal funds rate would fall to a range of 2.75% to 3.00%. There was even over a 25% probability that rates would drop further to a lower level.

2026 Rate Expectations (Screenshot from September 2025)

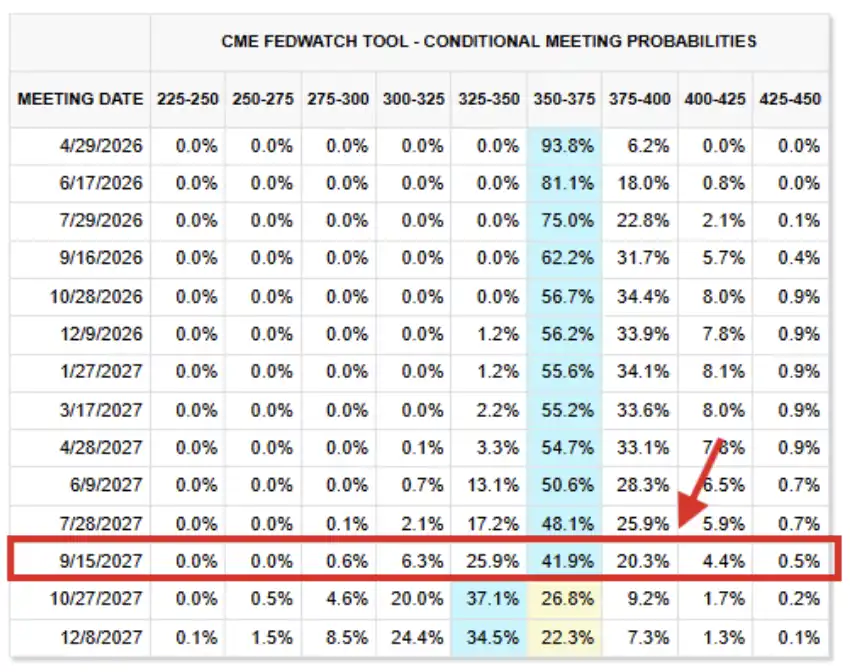

Now, looking at the current rate futures pricing. The present "base case scenario" indicates that rates will essentially remain unchanged at the current level until September 2027, with the Federal Reserve's federal funds rate expected to be in the 3.50% to 3.75% target range.

This level is 75 to 100 basis points higher than expected a few months ago, and this assessment has now been extended to the end of 2027.

Interest Rate Futures Situation as of March 26, 2026

In fact, the market has begun discussing the possibility of "rate hikes" again: currently, about 43% probability believes that the Fed will raise rates before the end of 2026. Objectively, the market can hardly withstand such an impact anymore.

Next, let's explain the reasons.

Labor Market Will Only Get Worse

On September 17, 2025, the Fed implemented a rate cut as widely expected by the market, hinting at two more rate cuts before the end of the year. At that time, despite inflation still significantly above the Fed's long-term 2.00% target, market concerns about the U.S. labor market were intensifying.

In the post-meeting statement, the FOMC described economic activity as "slowing" and added that "job growth has slowed," while noting that inflation "has risen and remains at a relatively high level." The weakening job market and rising inflation actually deviated from the Fed's dual goals of "stable prices" and "full employment," but at that time, labor market issues were more pronounced.

Today, the condition of the labor market has only worsened. Compared to September 2025, the current market's ability to withstand higher rates is actually weaker.

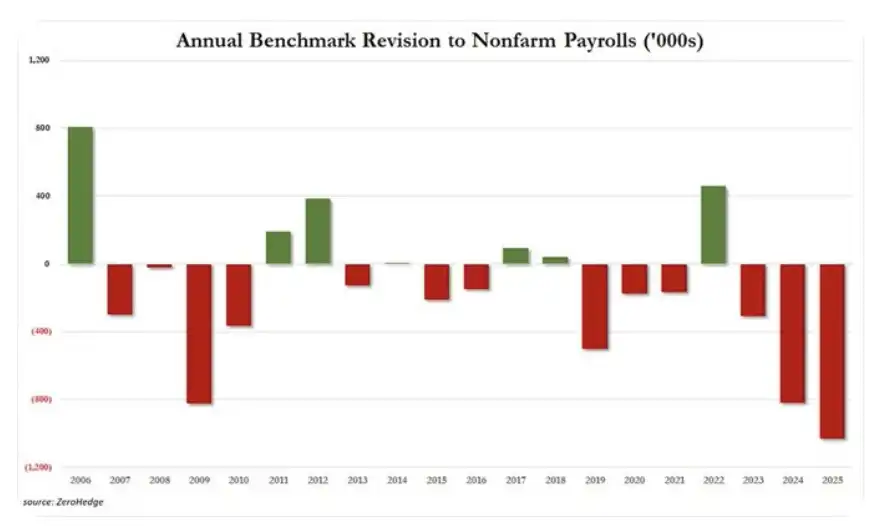

The reality is: first, the U.S. employment data for 2025 has been significantly revised downward by 1.029 million jobs, marking the largest annual downward revision in at least 20 years. Previously, the employment data for 2024 and 2023 were also revised down by 818,000 and 306,000 jobs, respectively.

Over the past three years, 2.153 million jobs have "disappeared" from the originally reported data. Since 2019, the total number of jobs revised away has reached 2.5 million, and over the past 7 years, 6 years have seen negative revisions to employment data.

Annual Revision Status of Nonfarm Payrolls

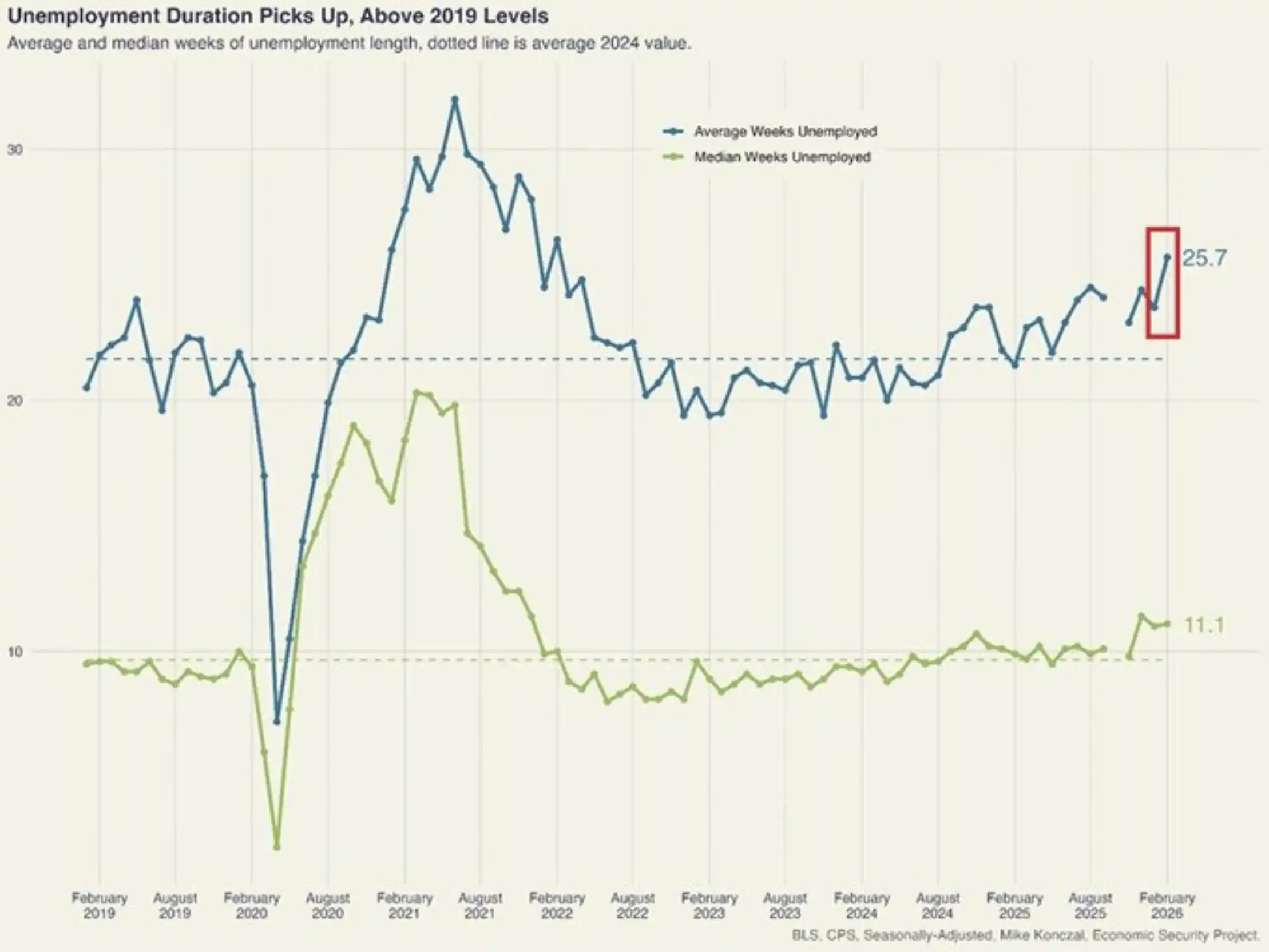

Another example, there are actually many similar cases. The average duration of unemployment in the United States increased by 2 weeks in February to reach 25.7 weeks, hitting a new 4-year high. Since October 2023, the duration of unemployment has increased by 6.3 weeks, the fastest pace since 2020 to 2021. This level is now significantly higher than the pre-pandemic levels of 2018 to 2019.

US Unemployment Duration Surges

Once again, this type of signal is far from unique, as we are seeing continued and escalating weakness in the labor market.

From our vantage point, the US economy is unlikely to withstand a 10-year Treasury yield approaching 4.50%, let alone rising above 5.00%.

Why is All This Happening?

At a macro level, the surge in US Treasury yields and the reversal of rate cut expectations can be attributed to one core variable: inflation.

The Fed's "dual mandate," established by the US Congress in 1977, requires the central bank to pursue two main objectives through monetary policy: maximum employment and price stability. As previously mentioned, when the Fed resumed rate cuts in 2025, the Federal Open Market Committee (FOMC) viewed the weakness in the labor market as "more important" than the still-elevated inflation.

However, with rising energy prices, the ongoing Iran conflict, and the post-war energy recovery cycle being continuously extended, inflation has once again become the primary concern—not because the labor market has improved, but because inflation itself has become more severe.

US 12-Month Inflation Expectation

As shown above, the US's 12-month inflation expectation has surged to 5.2%, reaching its highest level since March 2023. It is worth noting that this expectation reversal began in early January and rapidly accelerated following President Trump's threats against Iran, military buildup in the Middle East, and the strike on Iran on February 28.

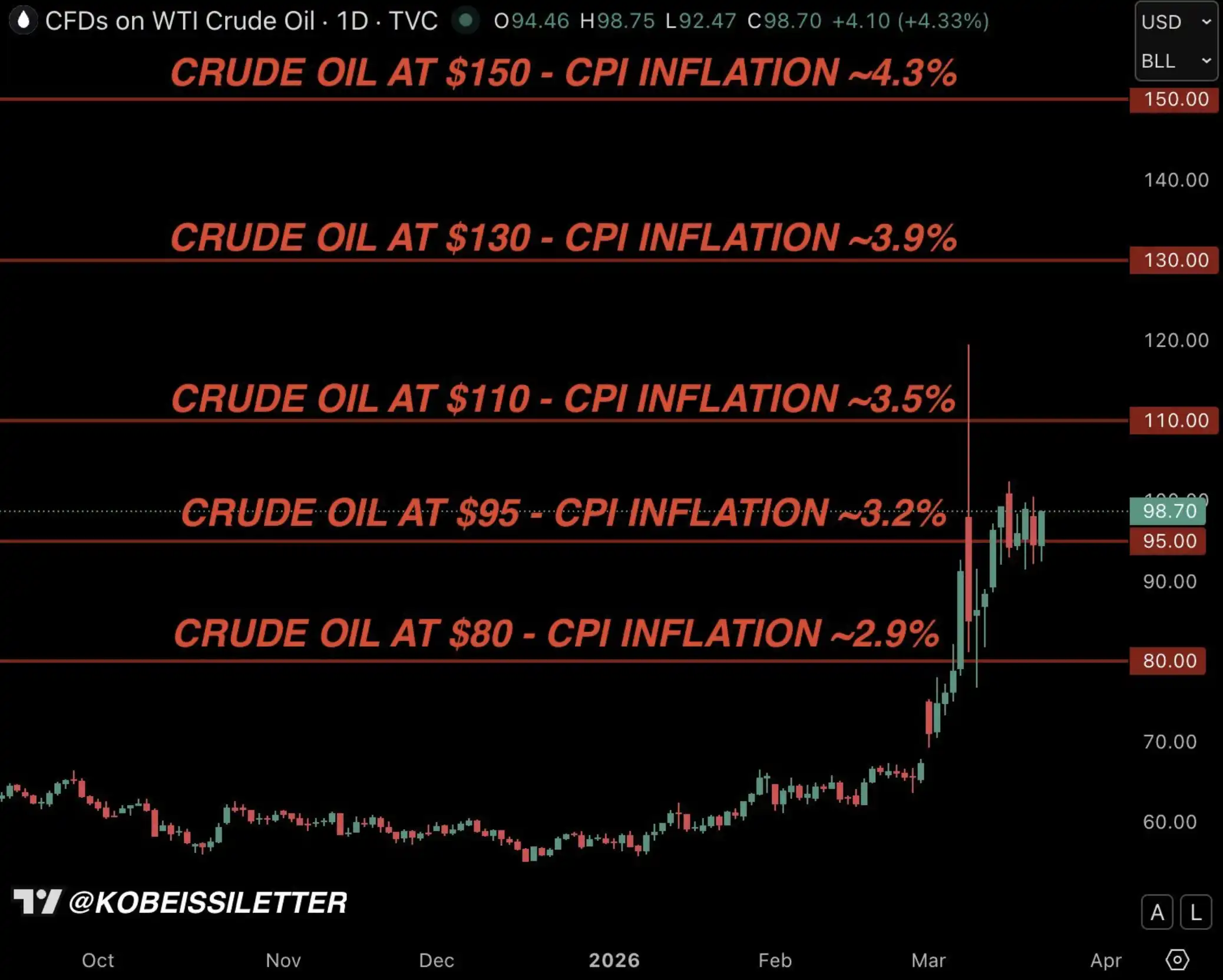

This brings us back to the CPI inflation chart based on model calculations below. As we have repeatedly emphasized since the outbreak of the war, if oil prices average $95 per barrel over a three-month period, US CPI inflation will rise to 3.2%.

Kobeissi Letter: US Oil Price and Inflation Model

However, in reality, considering the current series of chain reactions, the extent of inflation's upward movement is likely to be more than 3.2%.

We Believe "Intervention" Is Imminent

During the intense market volatility sparked by the early 2025 trade war, there was a key factor that ultimately led President Trump to announce a 90-day tariff suspension in April 2025—the bond market.

In the following chart, we have outlined the complete timeline of the uptrend in U.S. Treasury bond yields during the so-called "Liberation Day," which ultimately led to a policy shift on April 9, easing market pressures.

During an on-site interview on April 10, Trump also explicitly stated that he was closely monitoring the bond market's movements.

U.S. 10-Year Treasury Yield in April 2025

It can be seen that the U.S. 10-year Treasury yield in the range of 4.50% to 4.70% likely constitutes what we refer to as the Trump "Policy Shift Zone." This level is slightly above the current position, and we largely agree that once the yield reaches this range, policy intervention will become necessary to prevent a severe economic downturn in the U.S.

U.S. 10-Year Treasury Yield, Trump's "Policy Shift Zone"

In our view, this time will be no exception. In fact, we believe that President Trump's announcement of "peace talks" on March 23 was not a coincidence, as detailed below.

March 23, First Signal of Intervention

At 4:30 a.m. EDT on March 23, we pointed out that compared to the energy market, the bond market's issues had become more "disordered." Shortly after, just 2 hours later, the 10-year U.S. bond yield rose to 4.45%, indicating that President Trump likely had a decision-making discussion similar to April 9, 2025, when he announced a 90-day tariff suspension.

Another hour later, Trump announced a 5-day postponement of the strike on Iranian power facilities and stated that "productive" dialogue had begun between the U.S. and Iran aimed at ending the war.

This may have been the first signal of intervention.

What Should You Do Now?

The most common question we receive is: What does this mean?

From a macro perspective, we want to emphasize one point: the Trump administration is highly sensitive to fluctuations in the stock, commodity, and bond markets. This is good news for investors—Trump does not want market declines, and his level of concern on this issue is significantly higher than past administrations.

This is also why, after an initial surge in oil prices, there was still overall control. Crude oil investors generally believe that once the oil price approaches $120 per barrel again (as seen in the early stages of the war), Trump will quickly take intervention measures.

More broadly, we believe that as the 10-year U.S. Treasury yield rises, the downward pressure on the stock market will intensify; however, when the yield approaches the 4.50% to 4.70% range we mentioned, the upcoming policy shift or "intervention" will limit the downside of the stock market.

In addition, Trump, the Fed, and the entire government are aware that the U.S. labor market cannot sustain higher rates in the long term, which also means that the current situation is unlikely to evolve into a "long war," and it is more likely that some degree of moderation or resolution will occur in weeks rather than months.

Finally, behind these fluctuations and noises, we want to emphasize: the AI revolution is only accelerating. Those AI companies that have led the market since 2022 and are now under pressure due to a pullback are actually investing more and building faster.

Our outlook on the stock market and the long-term trend of AI has not changed.

Keep a Close Eye on the Bond Market

What we are experiencing is not just volatility, but a shift in "decision-making variables."

Over the past few weeks, the market's attention has been focused on oil prices, war news, and geopolitical escalations. But beneath the surface, a more powerful force is gathering strength and beginning to dominate the situation.

The bond market is redefining the direction of stocks, commodities, and even policies. And history has repeatedly shown that when financial conditions tighten too quickly, the question of intervention is never "whether it will happen" but "when it will happen."

As we have emphasized throughout this year, this market is increasingly resembling a game of "pattern recognition," with the key being to act one step ahead of the "crowd."

We believe the bond market will become the next most important narrative.

You may also like

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.